“We have a fuel price crisis, not a fuel supply crisis”.

That was the key takeaway from Steve West, the first of two speakers at Transporting New Zealand’s Fuel Pricing and Supply Seminar held in Wellington and online on 9 April.

Arranged to provide expert insight into what is happening with fuel prices and supply both domestically and globally, Steve joined us from local consultancy firm Envisory, who are experts liquid fuel supply chain logistics and infrastructure, procurement, and commodity pricing.

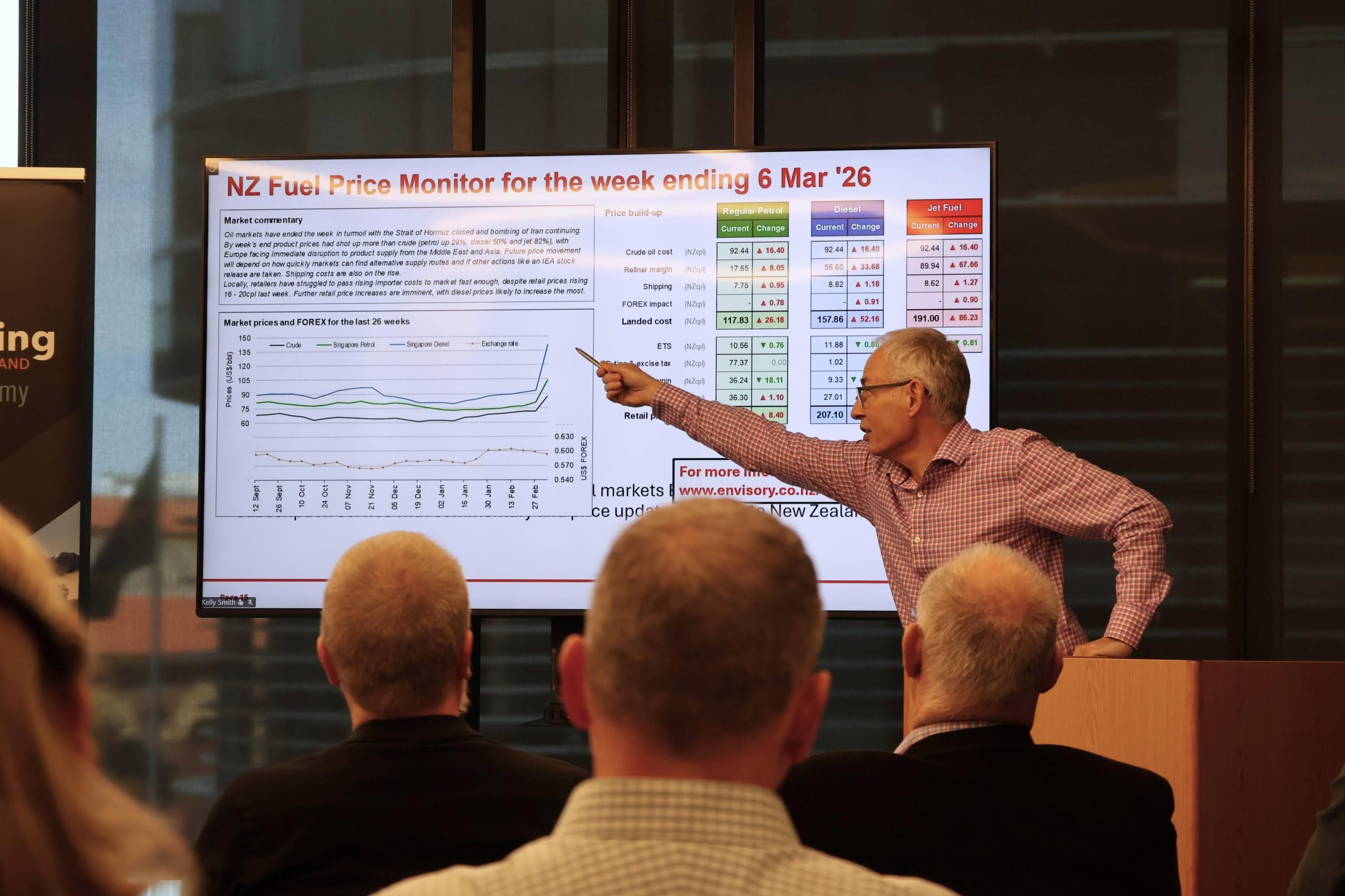

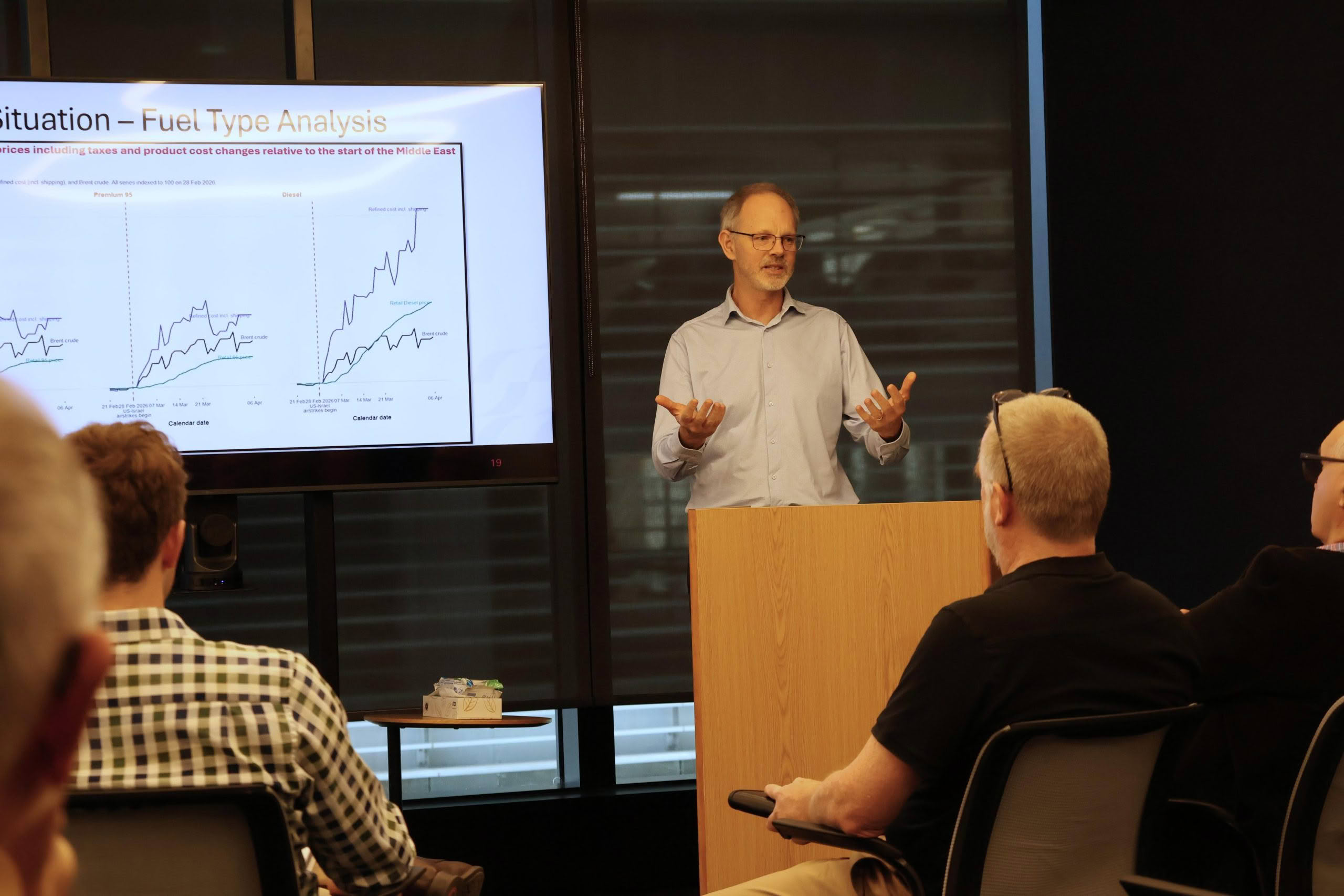

Steve outlined that the dramatic rise in the price of fuel has not been due to actual shortages – with shipments of diesel arriving about every two days in NZ – but rather a global market response, and also keenly illustrated that it is not the price of oil which has led to the huge jump in diesel prices in particular.

Steve’s presentation included some alarming graphs which showed that while oil prices have risen 50% (to as high as US$120/barrel) since the attacks on Iran, the benchmark commodity price for diesel supplied into our market had more than trebled to US$300/barrel. Curiously, petrol commodity prices have not jumped as high (to around US$150/barrel), which explains why petrol pump prices have not risen in sync with diesel here in NZ, and why diesel prices now surpass that of petrol at the pump – despite the fact that petrol has an additional 76 cents/litre of tax added onto it.

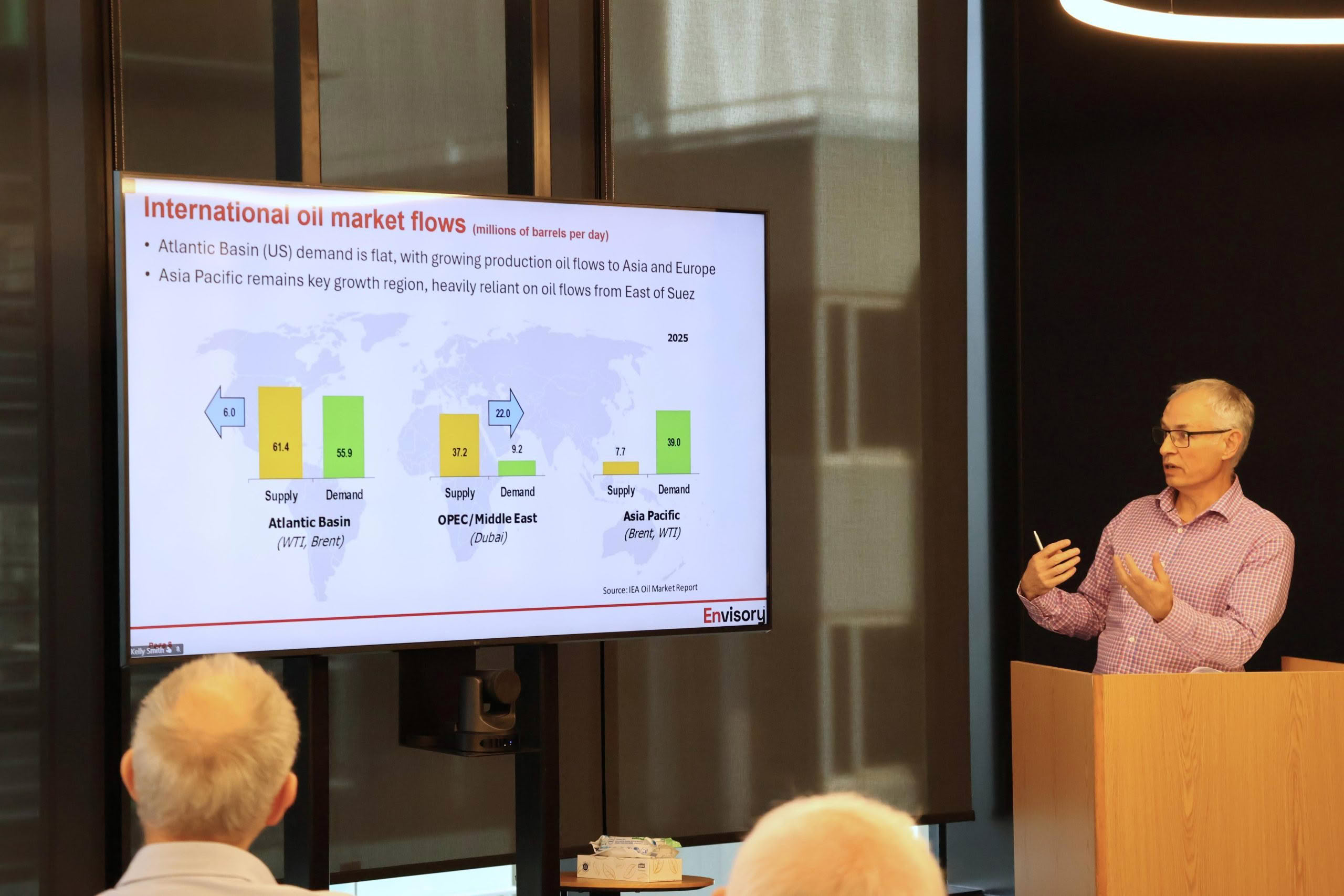

Steve noted that 85% of NZ’s fuel supply comes from southeast Asia, but most of the crude oil is sourced from outside Asia – much of it from the Middle East – so our region has been particularly hard hit by the Middle Eastern crisis. Other regions whose oil supplies exceed local demand have not been as badly affected, and their local commodity prices have not risen as much. The USA for example is a net oil exporter, and could be a potential alternative source of refined fuel into NZ.

Interestingly, Steve observed that if the Marsden Point refinery was still operating (which used to supply roughly half of NZs refined fuel needs), it could have been a hindrance in the current crisis, as it relied on Middle Eastern crude oil and so could have suffered supply shortages. Something he reiterated is not currently the case for the markets we now source all our fuel from. But Marsden Point is still operating as a storage facility, with some 300 million litres of storage, holding 40% of NZ’s fuel stocks.

All of this is cold comfort to truck operators who’ve experienced “unprecedented” jumps in the price of diesel, as Steve put it. The seminar’s second presenter, Bryan Chapple from the Commerce Commission, summarised their role in monitoring retail fuel prices, including truckstops. The Commission had observed that, prior to the current crisis, rural settlements and small rural urban areas tended to be more expensive than main urban areas, but that trend had since reversed. Their monitoring also saw that pump prices somewhat lagged the dramatic rises in commodity prices, with the fuel companies seemingly smoothing out some of the price shocks – even though it doesn’t feel like it.

Bryan also reiterated that companies should not discuss contract rates and fuel adjustment factors (FAF) with competitors, and that FAFs or fuel surcharges should only reflect actual changes in fuel prices, or otherwise they will breach the Fair Trading Act.

Seminar participants also heard why it is that pump prices rise so promptly, despite the fuel in service station tanks having been purchased at a lower price. Steve West explained that the fuel importers need to pay for the next shipment, at the current market price, and in order to remain solvent they need to recover that latest cost at the pump, Steve noting that the cost of a tanker of diesel for example has trebled from $25m to $75m.

In summary, the presenters illustrated that there is nothing untoward happening in the NZ retail fuel market, and that what we are experiencing is due to market forces outside local fuel companies and government control. But NZ and the Asia Pacific region has been hit especially hard. Perhaps one conclusion might be that NZ doesn’t need our own refinery to shield us from commodity price spikes, but rather our own source of oil?

- A recording of the seminar with PowerPoint presentation is available here.